What is a Deposit Return Scheme (DRS)?

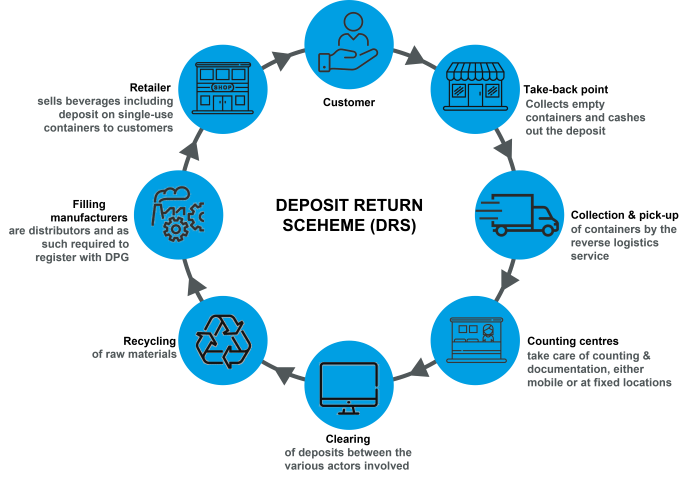

Deposit return schemes are used across the world as a way of encouraging more people to recycle drinks containers, such as bottles and cans. They work by charging anyone who buys a drink a small deposit for the bottle or can that it comes in. They get this money back when they return the bottle or can to a collection point to be recycled. Consumers will start paying a deposit at the point of purchase and redeem it through a reverse vending machine or designated return point. FDF member? Login or register for access to all the lastest updates and to find out how you can get involved. |

Find out more

Background

In early 2018, in the UK Government’s 25-Year Environment Plan for England, Defra committed to develop and consult on a deposit return scheme for drinks containers and, in late 2018, set out its objectives for a DRS in the Resources and Waste Strategy. In the 2019 manifesto, the UK Government committed to introducing a DRS in England. The Environment Act 2021 includes the primary powers required to deliver a DRS.

Two consultations have been held on developing a DRS.

- The first, in 2019, explored the design and scope that a DRS model could take.

- On 24 March 2021, the UK Government, the Welsh Government and the Department of Agriculture, Environment and Rural Affairs in Northern Ireland launched a second consultation on delivery of a DRS for single-use drinks containers.

Legislation and Consultations

Scope

- Size: The size of containers within scope of DRS will be 150ml to 3 litres. Any containers outside of this range will be in scope of the Extended Producer Responsibility for packaging (packaging EPR).

- This will apply in England, Northern Ireland and Scotland under the 3 nation DRS scheme.

- Material Scope: Polyethylene terephthalate (PET) bottles; steel and aluminium cans.

Deposit and Material Flows

- In setting producer registration fees, the DMO must consult with producers, and consider the size of the producer, based in part on the number of drinks containers that producer places on the market. The regulations will also require the DMO to publish its framework for calculating producer registration fees thereby ensuring fees are calculated transparently and appropriately.

- DMOs will recover the costs associated with operating DRS, including the fees charged to them by the relevant UK environmental regulators, through 3 key revenue streams:

- producer fees changed on a per container basis

- revenue from the sale of collected materials

- unredeemed deposits

- The DMO will have responsibility for setting the deposit level (fixed or variable), abiding by parameters set out in the regulations, including a maximum amount.

- Secondary legislation introducing the regulations will be introduced in due course and HMRC will also publish guidance on accounting for VAT on DRS supplies. The rules will ensure that VAT will only be collected on deposits that are not redeemed.

Deposit Management Organisation (DMO)

- The DMO(s) will be an independent, not for profit and private organisation(s). If more than one body is appointed, the regulations will place an obligation to coordinate their approach, where appropriate, such as in setting the deposit level.

- The Deposit Management Organisation(s) will be appointed through an application process set out in the regulations, as opposed to the competitive tender process proposed in the consultation. The DMO appointment period will be set out in the regulations, with longevity the favoured approach.

- The DRS’ obligated producers are brand owners or manufacturers of drinks in in scope containers that are then sold in England, Wales, or Northern Ireland, and includes those persons who import drinks containers to put on the market. Retailers are only considered to be a producer where they place own-brand drinks on the market in the relevant nation. Packaging manufacturers are also not included.

Implementation Timeline

The DRS will be an industry-led scheme implemented in three phases:

Phase 1: Regulation and Deposit Management Organisation(s) (DMO) appointment - by Spring 2025

Regulations in place in all administrations, and DMO(s) appointed.

Phase 2: Deposit Management Organisation (DMO) set-up - Spring 2025 to Spring 2026

This phase allows time to establish the DMO(s) as an organisation that is capable of running DRS on behalf of industry in each administration and providing businesses with the information needed to prepare for DRS launch.

This will include:

- securing funding and appointing key delivery partners, procuring IT and logistics or collection partners

- appointing CEO, leadership team and staff

- designing and publishing decisions on key operational areas

- developing a delivery plan and operational blueprint for obligated businesses

Phase 3: Roll out - Spring 2026 to Autumn 2027

This phase allows time for businesses to make the changes required for DRS.

This will include:

- the DMO(s) establishing the necessary national collection infrastructure, including counting and sorting centres, equipment and collection vehicles, recruiting staff and planning logistics routes, plus setting up the necessary digital and IT infrastructure for the registration and reporting of over 20 billion containers

- retailer activity to make decisions on return point locations and design, procurement and installation of reverse vending machines

- producer activity to develop labelling and artwork; make preparations for collecting data; make changes to invoicing systems

- commencement of consumer engagement campaigns

October 2027: DRS launch

Deposit Return Schemes across the UK are operational. Deposits are applied to in scope drinks containers, which can be redeemed upon return of the container for recycling.

Related topics

Collection Consistency

Understand the obligations on local authorities as well as business and other non-household municipal premises for collections of recyclable waste for each of the four nations of the UK.

Extended Producer Responsibility

Food and drink manufacturers are keen that the implementation of EPR is as successful as it can be and that the risk of disproportionate cost being passed through to consumers is minimised.

Ambition 2030: Packaging

This pillar outlines how we will contribute to the implementation of a world-class packaging recycling.